This article was featured in Maine Seniors magazine, March 2019

After nearly a decade of above average returns in the stock market, volatility and the first major correction in years have made many investors fearful and unsettled against a backdrop of global trade tensions, increasing interest rates in the U.S., slower growth forecasts and uncertainty in Washington.

Many retirees who are living off investment income are now asking… "Should I increase my allocation to bonds and lighten up on stocks?"

Before answering that question, it's important to understand bonds and their potential benefits. It’s also critical to know how bonds have behaved historically in good and bad markets. Then you can decide if it is worth the effort to bring more of them along for the retirement climb.

What is a bond?

Put simply, when you buy a bond you are making a loan to a company or government entity. The bond has a specified term during which you as the bondholder receive interest on the loan: with your initial investment returned to you at the end of the term (typically most bonds have 1 to 20-year maturities.)

What are the benefits of owning bonds?

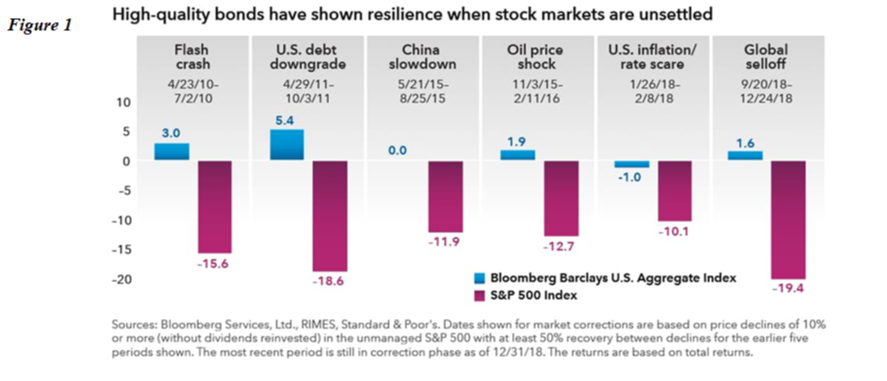

A major benefit of adding high quality bonds to a portfolio which is heavy in stocks is that bonds tend to rise or at the very least only fall slightly in a steep stock market selloff (see fig.1).

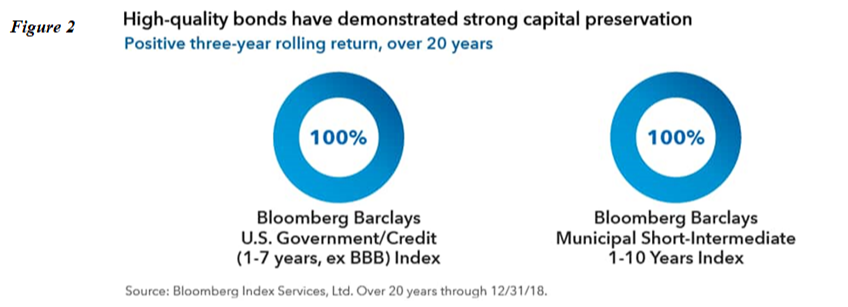

One mistake many investors and investment advisers alike make is having too much of their bond sleeve allocated to lower risk bonds. When investors panic, they look to reduce risk wherever they can find it, which means lower quality bonds can fall nearly as much as stocks. The core of most investors' bond portfolios should be in high quality U.S government and investment grade U.S. corporate bonds (see fig.2).

High income retirees who are Maine residents should also consider Maine municipal bonds which are exempt from both federal and state income taxes in most cases.

The second benefit of bonds is the income they generate to the bondholder. For a retiree or endowment withdrawing 3% -5% of their portfolio annually, we typically keep 7 to 10 years' worth of anticipated income in bonds—with slight adjustments to market conditions.

When growth stocks shrink, this allows you to have patience and not to panic and sell to the hungry bears appearing on the trail when the inevitable corrections and recessions hit.

Historically low interest rates have limited the appeal of bonds to many retirees over the last decade. With interest rates now rising, it has become a headwind for the stock market but possibly a chance to reduce risk and rebalance if you have too much in stocks.

Adding high quality bonds to a stock portfolio is like dragging along your gear, food and shelter when you are climbing a steep mountain which has a history of rapidly changing weather. You probably won't get to the top of the mountain as quickly, but your chances of hunkering down and surviving a bad mountain storm are much higher.

To each and every senior currently or about to climb that retirement mountain, it may be time to check in with your Sherpa to make sure you are adequately equipped to weather any future storms on your climb.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC.